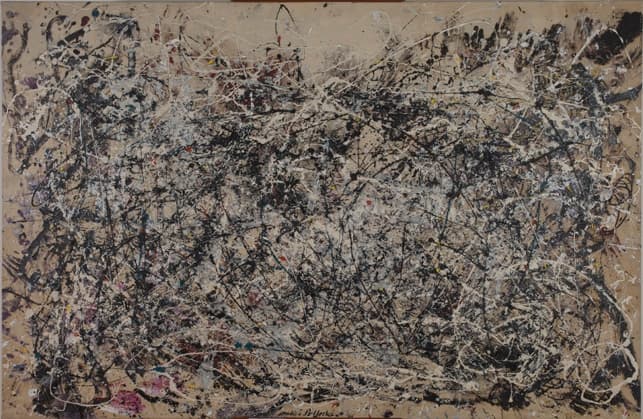

How Much Is Number 1A, 1948 Worth?

Last updated: May 7, 2026

Quick Facts

- Last Sale

- $3K (1950, Betty Parsons Gallery → Museum of Modern Art (acquisition; accession 77.1950))

- Methodology

- comparable analysis

Hypothetical market value for Jackson Pollock’s Number 1A, 1948 (MoMA accession 77.1950) is estimated at $100–150M. This reflects its canonical drip‑period importance, large scale, impeccable museum provenance and literature, and relevant private‑sale and auction comparables — but it remains a theoretical figure because the work is museum‑owned and has not been offered publicly since 1950.

Valuation Analysis

Estimate and basis: I place a hypothetical market band for Number 1A, 1948 at $100–150 million. This is a conservative‑to‑assertive private‑sale expectation for a large, museum‑quality Pollock drip canvas with MoMA provenance; it is calibrated against high‑end private‑sale anchors and public‑auction realizations for 1948–49 drip works and adjusted for condition/provenance advantages a museum ownership confers [1][2].

Comparables and anchors: Public‑auction top realizations in the last decade for canonical late‑1940s Pollocks sit in the $50–60M range (e.g., Number 19, 1948; Number 31, 1949) and illustrate the reliable auction floor for museum‑grade examples, while reported private sales (notably No. 5, 1948 in 2006) show how blue‑chip private transactions can push well above $100M in favorable circumstances [2][3]. The $100–150M band is chosen to reflect a credible private‑sale outcome (premium for rarity, institutional provenance and literature) while recognizing the more conservative public‑auction outcomes.

Provenance, condition and market impact: Number 1A’s continuous MoMA ownership since c.1950, documented acquisition from Betty Parsons, and extensive exhibition/literature presence materially strengthen attribution and market confidence; those positives justify upward pressure versus an anonymous private provenance [1]. Conversely, the painting has a documented conservation history (smoke/soot damage from a 1958 gallery fire and subsequent treatment) that must be transparently evaluated; with excellent restoration documentation the impact is neutral to modest, but any unresolved condition issues could reduce realizable price [1].

Liquidity and saleability: Because MoMA owns the work, any real sale would most likely be a highly public deaccession or an extraordinary institutional/private arrangement; the buyer pool for nine‑figure Pollocks is small (museums, ultra‑high‑net‑worth collectors, sovereign/major foundations), which both supports high prices for exceptional works and limits liquidity. Public auction would likely produce more conservative realized numbers (based on recent houses’ results), whereas a discreet private placement could achieve the top of the band given competitive buyer interest and favorable timing [2][3].

Practical next steps: For an insured or transactional value: obtain MoMA’s latest full condition/conservation report, commission written pre‑sale estimates from two major houses (Sotheby’s/Christie’s), and prepare a modern provenance & literature dossier. If your objective is an insurance replacement value, ask MoMA or a specialist appraiser for a formal valuation — replacement figures can differ materially from hypothetical market estimates.

Key Valuation Factors

Art Historical Significance

High ImpactNumber 1A, 1948 sits squarely within Pollock’s canonical drip period (late 1940s), the moment most closely associated with his global reputation. As a large-scale, mature drip canvas from 1948 it exemplifies the technical innovations and cultural impact that make Pollock central to Abstract Expressionism. Works from this year are prioritized by museums and top collectors, and inclusion in MoMA’s holdings cements the painting’s scholarly status. That status translates directly to market value: canonical, well‑exhibited examples command the greatest scarcity premium because they are the works that define the artist’s market and institutional narratives.

Provenance & Exhibition History

High ImpactContinuous MoMA ownership since the 1950 acquisition (from Betty Parsons) provides exceptional provenance clarity and enhances buyer confidence. Long museum tenure means documented exhibition history, catalog inclusion and direct access to institutional records — all of which reduce attribution risk and encourage higher bids in private sales. Museum provenance is a primary driver when lifting a work into nine‑figure territory; buyers pay a premium for the certainty and prestige that comes with a leading institution’s stewardship.

Condition & Conservation

Medium ImpactThe painting has a documented conservation history, including smoke/soot damage from a 1958 gallery fire and subsequent treatment documented by MoMA. Well‑recorded, professional conservation generally mitigates buyer concern, but any residual structural or surface issues would be value‑diminishing. A current, detailed condition report (including technical imaging and materials analysis) is essential: if the canvas is structurally sound and the restoration is well‑documented, condition should not materially reduce the estimate; unresolved or intrusive interventions would lower realizable value.

Market Comparables & Demand

High ImpactRecent public auction results for late‑1940s Pollocks set a conservative benchmark (examples selling in the $50–60M range), while reported private transactions (e.g., the widely cited 2006 sale of No. 5, 1948) demonstrate that nine‑figure private deals are possible for prime canvases. These comparables create a two‑tier market: robust auction floors and a higher private‑sale ceiling. The $100–150M band reflects a plausible private‑sale outcome for a museum‑grade Number 1A, recognizing both the auction evidence and private‑sale upside.

Liquidity & Marketability

Medium ImpactThe buyer universe for a nine‑figure Pollock is narrow (major museums, prominent private collectors, foundations), which supports high pricing but limits immediate liquidity. MoMA ownership further constrains marketability because institutional deaccessions are rare and closely regulated; any sale would be exceptional and highly public. For a private seller the path to top‑end realization typically runs through discreet negotiation with several potential buyers, whereas a public auction could produce a lower but more certain outcome.

Sale History

Betty Parsons Gallery → Museum of Modern Art (acquisition)

Jackson Pollock's Market

Jackson Pollock is among the most valuable American postwar artists; his late‑1940s and early‑1950s drip canvases are the marquee segment of his market. Blue‑chip collectors and museums prize canonical drip works, producing a persistent demand that supports high pricing. The market exhibits a two‑tier behavior: consistent multi‑million auction floors for authenticated works and occasional private‑sale outliers that can exceed public records. Pollock remains a cornerstone of institutional collections and a sought‑after name in major private transactions.

Comparable Sales

No. 5, 1948

Jackson Pollock

Top-tier late‑1948 drip canvas; widely cited private‑sale high‑water mark for Pollock and an important market anchor for 1948 drip works.

$140.0M

2006, Private sale (reported; widely reported 2006 transaction)

~$224.0M adjusted

Number 19, 1948

Jackson Pollock

Major 1948 drip canvas sold at auction (world auction record context); directly comparable by period/style and scale.

$58.4M

2013, Christie's New York

~$80.5M adjusted

Number 31, 1949

Jackson Pollock

Recent high‑level auction result for a late‑1940s Pollock drip canvas; close in market standing to other auctioned major drip works.

$54.2M

2022, Christie's New York

~$59.6M adjusted

Untitled (c. 1948)

Jackson Pollock

Mid‑range authenticated drip‑period Pollock sold at a major house—useful to gauge the mid‑tier market for similar works.

$15.3M

2024, Phillips New York

~$15.6M adjusted

Current Market Trends

The blue‑chip postwar/modern market remains selective but resilient. Recent years have shown continued appetite for museum‑quality examples even as mid‑tier demand fluctuates. Private sales continue to produce headline outliers that lift perceived ceilings, while public auctions provide a reliable floor. Macroeconomic factors (rates, liquidity) and collector concentration influence timing and pricing; for Pollock, top examples retain strong long‑term value.

Sources

- MoMA collection record: Jackson Pollock, Number 1A, 1948 (accession 77.1950)

- Christie's press release and auction results (Number 19, 1948; Number 31, 1949) and related auction coverage

- UPI report (widely cited) on reported private sale of No. 5, 1948 (2006)

- MoMA conservation project notes for Number 1A, 1948

- Market coverage of recent Phillips and secondary‑market Pollock sales (example coverage)