Most Expensive Jackson Pollock Paintings

Jackson Pollock’s oeuvre occupies a singular, almost mythic place in the art market: his large-scale, drip paintings are both touchstones of Abstract Expressionism and perennial blue-chip investments, commanding staggering sums that reflect their cultural and historical weight. At the pinnacle sits Number 1, 1950 (Lavender Mist), valued in the roughly $150–350 million range, while No. 5, 1948 has been estimated between $220–300 million, signaling how scarcity and provenance can drive astronomical prices. Works like One: Number 31, 1950 ($150–250 million) and Autumn Rhythm (Number 30) ($100–150 million) show that scale, condition and exhibition history translate directly into market standing. Mid-tier masterpieces such as Number 19, 1948, Number 1A, 1948 and Number 32, 1950 (each roughly $100–150 million) sit just below the stratospheric sales, with later pieces like Number 17, 1951 ($60–85 million) and Number 31, 1949 ($45–70 million) still commanding significant sums. Collectors prize Pollock for his revolutionary technique, provenance, and the way each canvas reads as both object and event—qualities that continue to make his paintings highly collectible and fiercely sought after.

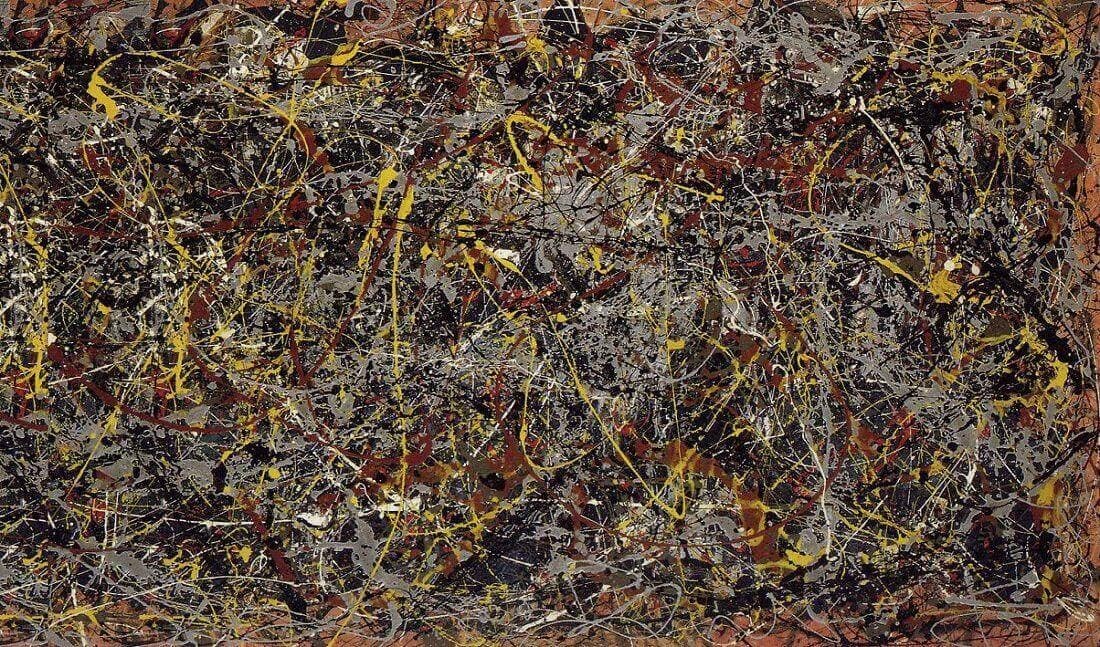

$150-350 million

As the National Gallery of Art’s canonical Pollock, Lavender Mist would command a private‑market trophy premium, estimated at USD 150–350 million based on private and auction benchmarks.

$220-300 million

No. 5, 1948’s extreme scarcity yields a USD 220–300 million private‑sale valuation, extrapolated from Pollock’s $61.2M auction record and the reported ~$200M private sale of Number 17A.

$250-300 million

Anchored to the widely reported ~$200 million private sale in 2015 and adjusted for 2026 purchasing power and market depth, Jackson Pollock’s Number 17A, 1948 is estimated at $250–300 million today.

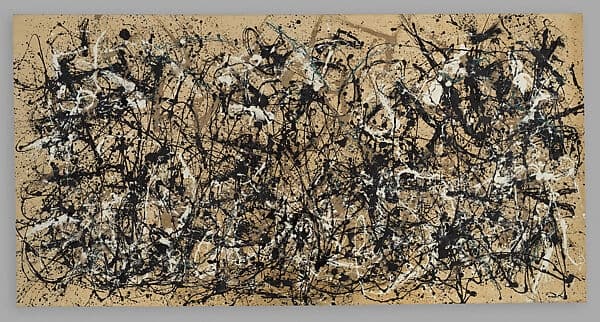

$150-250 million

Museum‑held One: Number 31, 1950 would sit atop the Pollock market, with a reasoned private‑sale range of approximately USD 150–250 million based on public and private anchors.

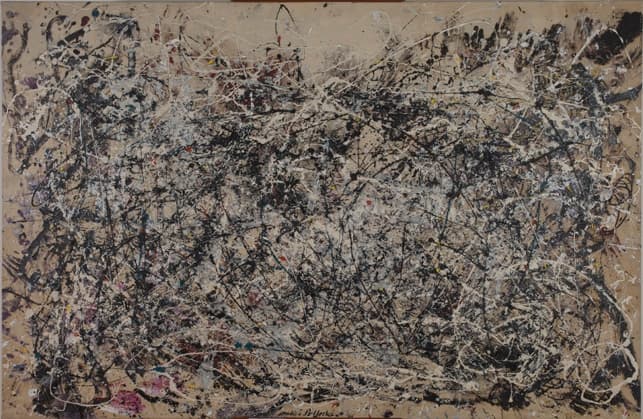

$100-150 million

Metropolitan Museum’s Autumn Rhythm is effectively off‑market but would command roughly USD 100–150 million under optimal sale mechanics and market conditions.

$100-150 million

MoMA‑accessioned Number 1A, 1948 is theoretically valued at USD 100–150 million, reflecting its canonical status, impeccable museum provenance, and relevant private‑sale and auction precedents.

$100-150 million

Number 32, 1950 (Kunstsammlung NRW) is a monumental, museum‑quality Pollock with a conservative presale estimate of USD 100–150 million based on auditable public‑auction precedent.

$100-150 million

Number 19, 1948’s USD 100–150 million estimate extrapolates from its 2013 Christie’s result and assumes pristine condition, clear title, and competitive private or institutional demand.

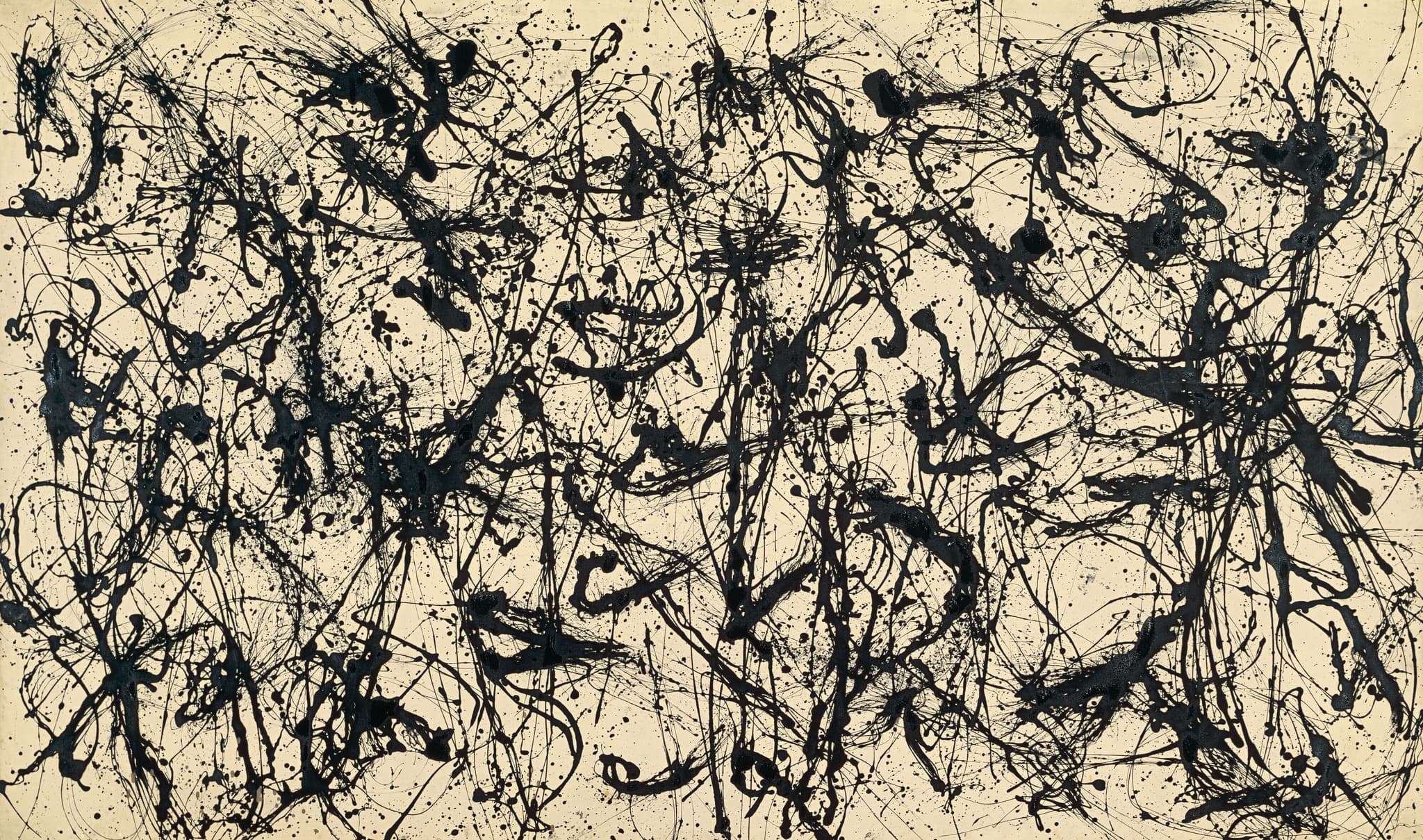

$60-85 million

Anchored by its Nov 15, 2021 Sotheby’s hammer-plus‑premium of $61.16M, Number 17, 1951’s defensible current‑market range is USD 60–85 million.

$45-70 million

Number 31, 1949 sold for $54,205,000 at Christie’s New York on 12 May 2022, which anchors today’s fair‑market range of approximately USD 45–70 million.

What Drives Value in Jackson Pollock's Work

Breakthrough late‑1940s to 1950 mature drip period

Pollock’s market premium clusters tightly around his 1947–50 breakthrough: canonical drips from 1948–1950 (No. 5, Number 19, Number 1A, Lavender Mist, One: Number 31) are valued far above earlier or later works. These years represent the technical and cultural apex of his poured technique; collectors explicitly pay for that historical moment. Sales evidence shows public auction anchors in the $50–60M range and private‑sale ceilings that escalate for works dated to this narrow, high‑demand window.

Monumental ‘all‑over’ scale as a multiplier

Very large, ‘all‑over’ canvases—Autumn Rhythm, Lavender Mist, Number 32—carry an outsized premium because Pollock’s compositional impact is inseparable from scale. Monumental size both signals museum quality and restricts buyer pool to institutions or ultra‑wealthy collectors, which intensifies competition when such canvases appear. The market routinely prices canvas size as a decisive multiplier for Pollock: the biggest mature drips sit at the top of the public auction band and approach private‑sale trophy pricing.

Support and technical/material type (canvas vs fiberboard vs paper)

Pollock’s choice of support materially alters value: works on canvas command the highest confidence; fiberboard pieces (e.g., No. 5’s support issues) and paper mounted on Masonite (smaller Number 31 examples) introduce conservation risks that suppress top bids. Buyers factor medium‑specific stability, relining history and varnish/enamel behavior into pricing. Proven conservation dossiers or problematic supports have respectively unlocked or constrained nine‑figure outcomes in comparable sales.

Pollock‑specific provenance concentration (museum holdings vs marquee private owners)

A distinctive Pollock pattern is where the best examples already reside: major museums (MoMA’s One: Number 31, Met’s Autumn Rhythm, NGA’s Lavender Mist, Kunstsammlung NRW’s Number 32) both confer prestige and remove supply, compressing market availability. Conversely, when prime drips are held by marquee private collectors (Ossorio, Newhouse, Geffen) they can trigger blockbuster private transactions. Thus provenance both elevates intrinsic desirability and determines whether a work can reach the private‑sale ceilings documented for top Pollocks.

Market Context

Jackson Pollock remains a blue‑chip, canonical post‑war master whose marquee drip canvases command the highest prices in the category: the public auction record stands at $61.2M (Number 17, 1951), while widely reported private transactions have implied ceilings in the low‑to‑mid hundreds of millions (e.g., Number 17A, reported ~ $200M). Supply of museum‑quality Pollocks is extremely limited, concentrating global demand among ultra‑high‑net‑worth collectors and leading institutions and driving a premium for fresh, exhibition‑worthy works. Since 2023 the ultra‑top segment cooled, with fewer headline $100M+ auctions and a shift toward curated private treaties, guarantees and brokered placements; a selective rebound emerged in late 2025. Macroeconomic conditions, philanthropic/institutional buying and exhibition timing will remain decisive for any prospective sale.