How Much Is Not to Be Reproduced Worth?

Last updated: March 18, 2026

Quick Facts

- Methodology

- comparable analysis

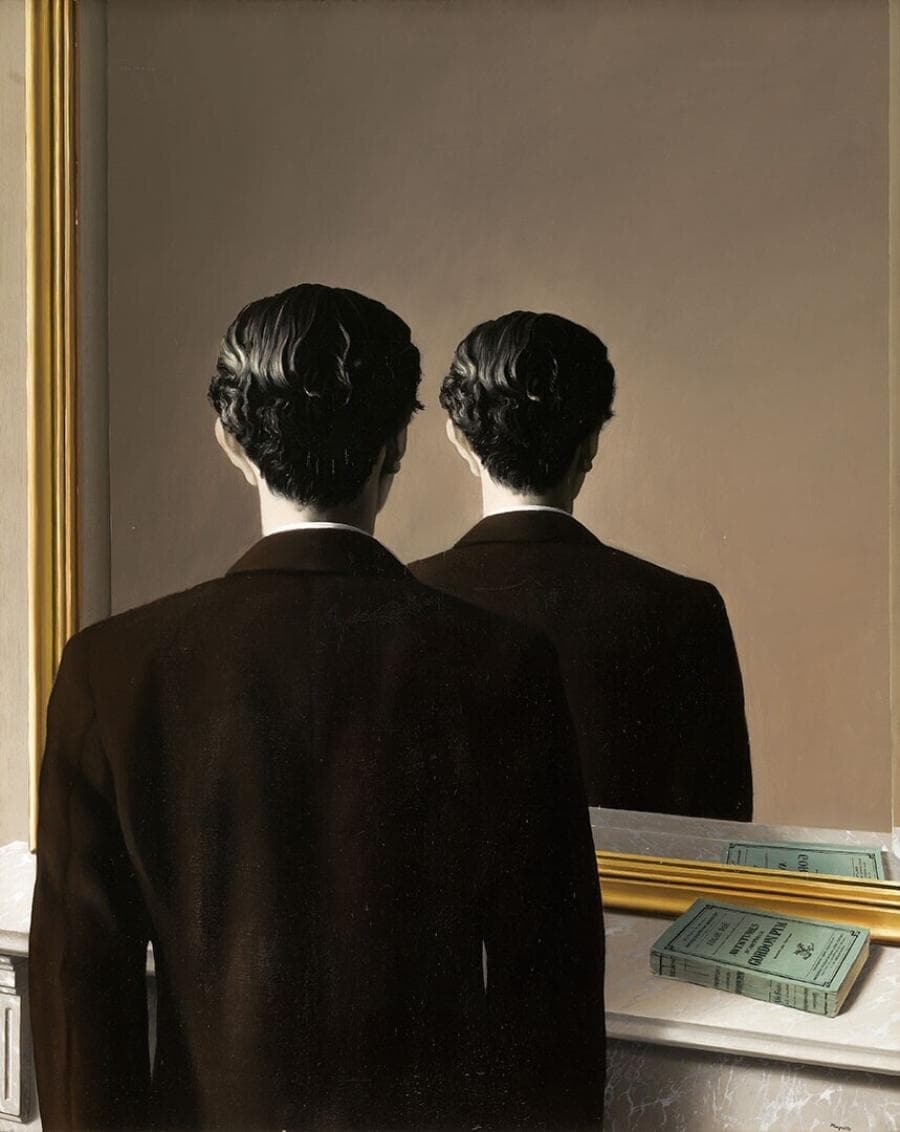

If this is the canonical 1937 oil La Reproduction interdite (museum example), it is not market‑traded today; hypothetically, a well‑provenanced, good‑condition 1937 Magritte of this importance would reasonably be estimated at $20–40M on the open market. If the object is a later studio version, print, or heavily restored piece, value drops to roughly $0.5–5M.

Valuation Analysis

Valuation conclusion: Based on market comparables for Magritte’s 1930s canonical oils and the rarity of such works coming to auction, a realistic traded‑market estimate for a primary, well‑provenanced 1937 oil of La Reproduction interdite is approximately $20–40 million. This bracket assumes secure attribution to René Magritte, intact original paint and medium, complete provenance and a sound conservation history.

The specific, canonical 1937 canvas is in the collection of Museum Boijmans Van Beuningen (acquired 1977) and therefore carries no modern public auction price; that museum holding removes it from the supply pool and is the principal reason the work itself has no sale history to reference directly [1]. In the absence of a direct sale, valuation rests on closely comparable 1930s Magritte oils and headline auction precedents.

Direct market precedent includes Magritte’s 1937 Edward James commission Le Principe du plaisir, which realized $26,830,500 at Sotheby’s New York in November 2018 and is the closest transactional analogue for a high‑quality 1937 Magritte canvas in private hands [2]. More recent headline results for exceptionally rare Magrittes (notably L’empire des lumières variants) have established a substantially higher ceiling in exceptional circumstances, demonstrating both strong demand and a wide value dispersion at the top end of the market [3].

Primary value drivers are: confirmed attribution to the 1937 canonical version (and any Edward James commission link), the completeness and reliability of provenance and exhibition history, the painting’s physical condition and conservation record, and sale channel (major evening sale vs private treaty). When these align positively, the $20–40M band is supportable; if one or more are compromised (uncertain attribution, major restoration, provenance gaps), the value can fall sharply to the mid‑six‑figure or low‑seven‑figure range typical for studio copies, later replicas or prints.

For a firm market valuation and sale strategy: obtain catalogue‑raisonné confirmation, a full provenance and exhibition bibliography, high‑resolution photography and a professional conservation/technical report, then request formal conditional estimates from the Impressionist/Modern and 20th‑century Surrealism specialists at Sotheby’s, Christie’s and Phillips. Those parties will refine the range, advise sale timing and channel, and produce a written pre‑sale estimate appropriate for auction or private sale.

Key Valuation Factors

Art Historical Significance

High ImpactLa Reproduction interdite (the man facing a mirror that reflects the back of his head) is a distinctly iconic Magritte motif from his mature 1930s Surrealist period. As a recognized image in scholarship and exhibition history, the canonical 1937 oil carries substantial cultural and curatorial weight. Works that articulate key motifs from an artist's peak period command premium interest from museums and blue‑chip collectors because they are both visually emblematic and historically important. That imprimatur elevates bidding competition and institutional interest, and it is a primary reason a fully authenticated original would sit in the tens of millions.

Provenance & Exhibition History

High ImpactComplete, documented provenance (especially a direct commission or early ownership by a known collector such as Edward James) and demonstrable exhibition/bibliographic history materially increase market value and buyer confidence. Museum acquisition and long‑term public display further validate authenticity and scholarly importance; the canonical 1937 canvas’ Boijmans accession is an example of how institutional ownership removes supply and enhances the theoretical market value. Conversely, gaps in provenance, unclear title history, or controversial ownership transfers reduce marketability and can significantly depress realized prices.

Condition & Conservation

High ImpactThe painting’s physical state—original paint layer integrity, degree and quality of past restoration, varnish discoloration, relining, flaking, or inpainting—directly affects value. A technically healthy, minimally restored canvas will outperform one with heavy intervention. Technical imaging (X‑ray, IRR, pigment analysis) often resolves attribution and dating questions; conservation reports can both reassure buyers and set limitations on insurability and export. Degraded condition or invasive restoration can reduce market value by a large percentage, sometimes moving a work from multi‑million to low‑million status.

Market Comparables & Auction Record

High ImpactComparable sales provide the primary empirical basis for the estimate. A directly relevant sale is Le Principe du plaisir (1937) at Sotheby’s New York in 2018 (≈ $26.8M), which supports a mid‑tens of millions anchor for canonical 1937 oils. Recent record sales of other Magritte masterpieces show the market ceiling for exceptionally rare works is substantially higher, but such results are reserved for uniquely sought motifs, provenance and condition. Auction house estimates, buyer premium structures, and private‑sale benchmarks all inform the final pricing and recommended sale channel.

Rarity & Availability

Medium ImpactMuseum holdings and a limited number of high‑quality 1930s Magritte oils create scarcity. When a museum‑quality, iconic Magritte does become available, multiple institutional and private bidders typically compete, compressing supply and supporting premium pricing. However, Magritte also produced later studio versions and numerous prints; distinguishing the canonical original from later versions is critical because those variants are far more common and trade at substantially lower price tiers. The interplay of rarity and documented authenticity therefore materially influences realized value.

Sale History

Not to Be Reproduced has never been sold at public auction.

Rene Magritte's Market

René Magritte is firmly established as a blue‑chip Surrealist: his best 1930s–1950s oils regularly attract major institutional buyers and wealthy private collectors. Auction records have expanded in recent years, with several headline sales pushing artist ceilings into the tens of millions and, on rare occasions, into the eight‑figure range. Typical realized prices vary widely by period, size, and subject: canonical museum‑quality canvases from the 1930s achieve the highest levels (tens of millions), while studio works, prints and studies are priced much lower. Strong global demand and collector recognition underpin liquidity for top examples.

Comparable Sales

Le Principe du plaisir

René Magritte

Same artist and same year (1937) as La Reproduction interdite; an Edward James commission and a direct precedent for market value of top‑tier 1937 Magritte oils.

$26.8M

2018, Sotheby's New York

~$33.5M adjusted

L'empire des lumières

René Magritte

Major, museum‑quality Magritte masterpiece sold at a very high level; while a different motif/series, it demonstrates demand and the market ceiling for top Magritte oils.

$78.0M

2022, Sotheby's London

~$82.7M adjusted

L'empire des lumières (another version)

René Magritte

Record‑setting Magritte at auction (Nov 2024) — shows upside for the very rarest, most iconic Magritte oils; useful as an upper‑end benchmark.

$121.2M

2024, Christie's New York

~$124.8M adjusted

Current Market Trends

The market for top‑tier 20th‑century Surrealism and Magritte remains robust, with strong institutional interest and record results in headline auctions. That said, pricing is concentrated at the very top for museum‑quality pieces and can be sensitive to macroeconomic factors and auction calendar timing. Private treaty sales are increasingly used for ultra‑high‑value works to manage buyer anonymity and strategic pricing.