Most Expensive Rene Magritte Paintings

Rene Magritte occupies a singular position in the modern art market, where surrealist wit, graphic clarity, and an enduring visual vocabulary have made his canvases highly collectible and consistently sought after by museums and private collectors alike. At the apex sits This is Not a Pipe, estimated between $160–220 million, a work whose paradoxical title and crisp trompe-l’œil logic encapsulate Magritte’s philosophical charm and explains its extraordinary market standing. Equally emblematic are The Lovers ($120–170 million) and The Empire of Light and The Son of Man (each around $100–150 million), paintings whose iconic imagery—veiled faces, nocturnal skies over sunlit streets, and enigmatic apples—translate readily into cultural currency and institutional desire. Lower but still impressive price bands, from Time Transfixed ($30–80 million) and The Pleasure Principle ($30–50 million) to Golconda and The Menaced Assassin (roughly $20–60 million), reflect strong demand for signature motifs across scales. Even works with broader estimates like Not to Be Reproduced ($20–40 million) and The False Mirror ($10–40 million) confirm that Magritte’s blend of conceptual rigor, visual immediacy, and historical significance continues to command top-tier auction results.

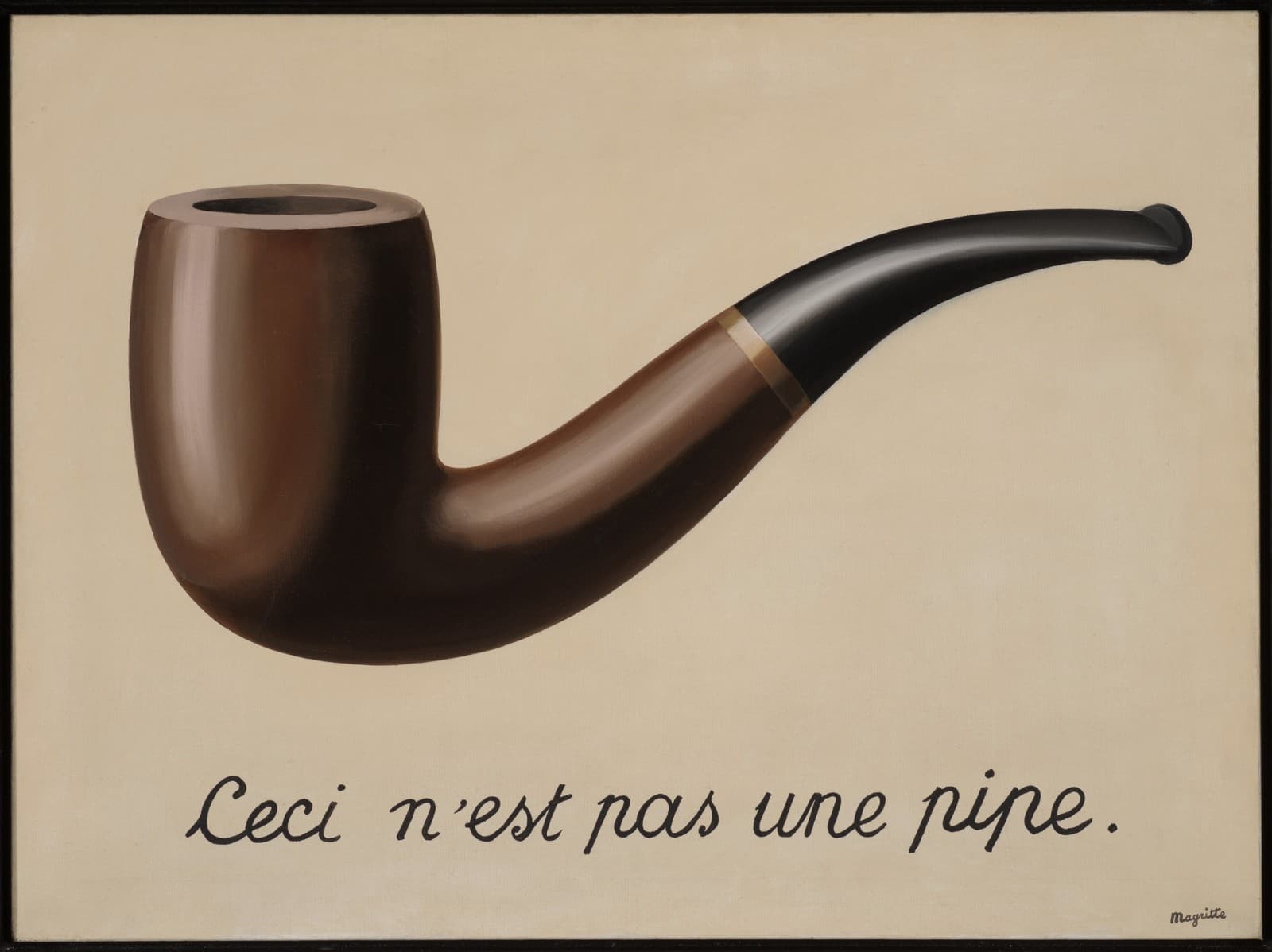

$160-220 million

The estimate exceeds Magritte’s $121.2M auction record, reflecting The Treachery of Images’ singular canonical status and near‑zero supply of true equivalents.

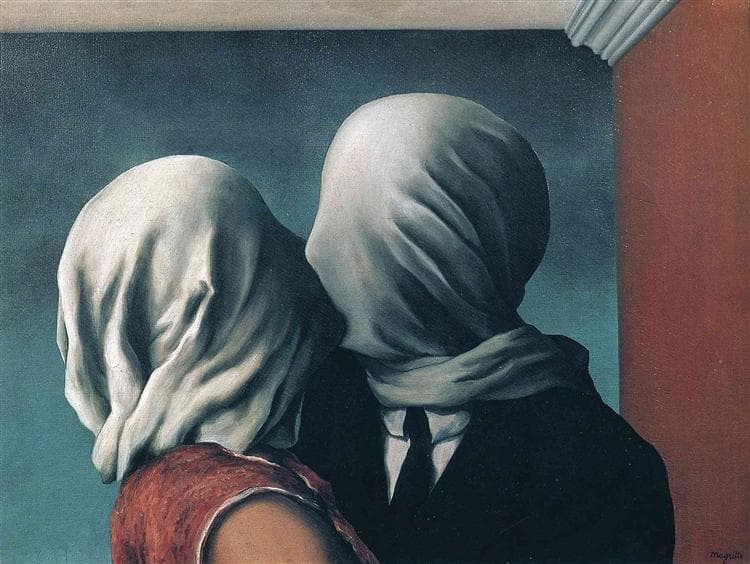

$120-170 million

MoMA’s 1928 The Lovers carries a premium over Magritte comparables because its prime date and image‑defining status make it virtually irreplaceable.

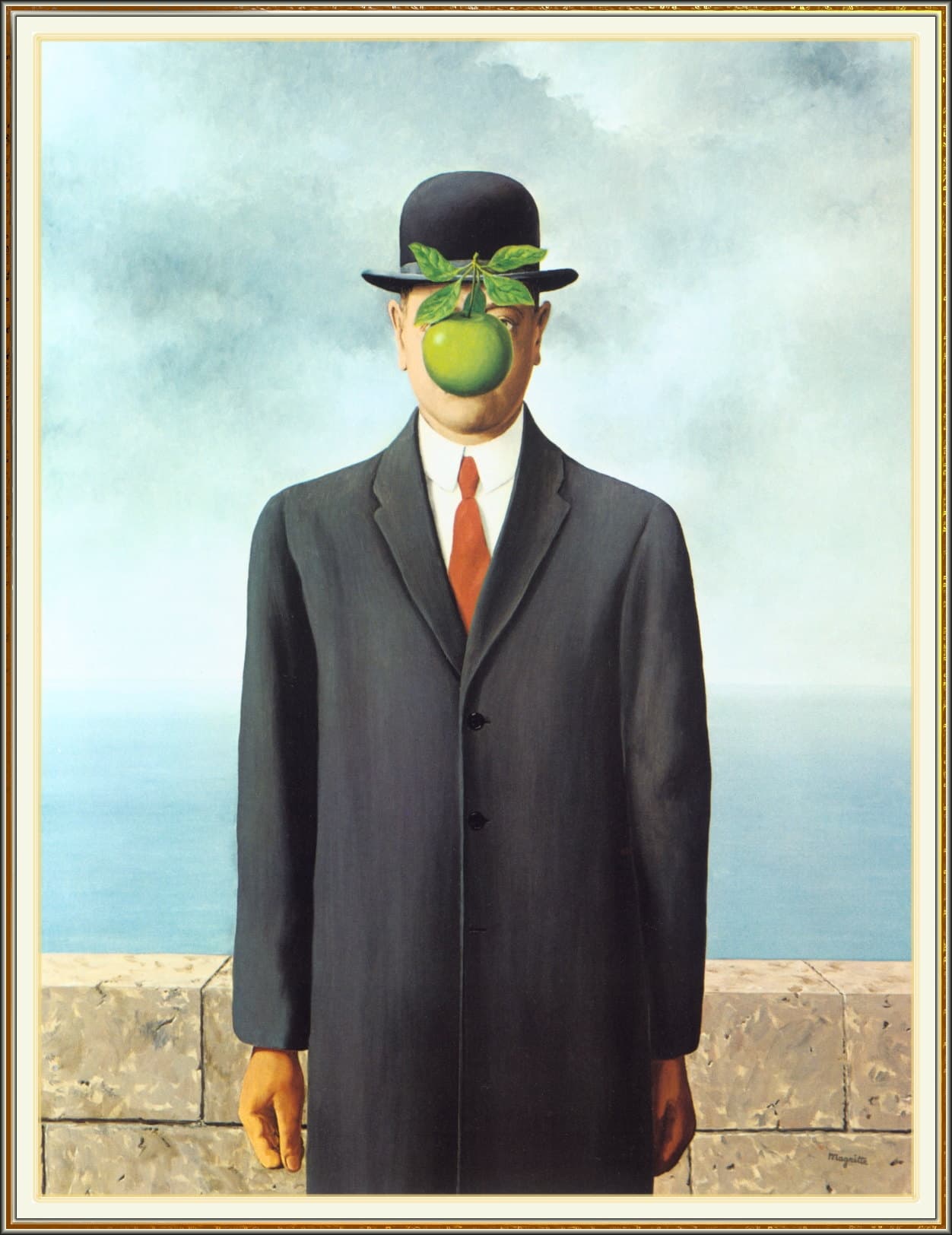

$100-150 million

Commissioned by Harry Torczyner and last sold at Christie’s in 1998 for $5.392M, The Son of Man’s iconic scarcity supports nine‑figure pricing atop Magritte’s $121.16M record.

$100-150 million

This range is calibrated to the Christie’s 19 Nov 2024 trophy sale and adjusts for museum‑quality size, condition, provenance, and catalogue‑raisonné confirmation.

$100-140 million

A prime, early-1930s oil-on-canvas from René Magritte’s canonical Human Condition series is valued at $100–140 million.

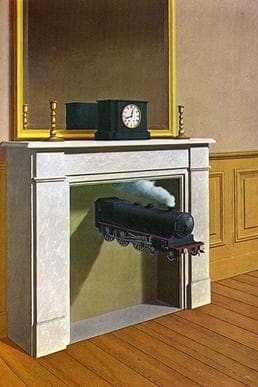

$30-80 million

Held by the Art Institute of Chicago and never sold publicly in modern times, Time Transfixed’s hypothetical auction outcome most likely sits mid‑range (≈$35–60M).

$25-60 million

The Menil’s canonical Golconda is effectively off‑market; a clean‑titled, well‑conditioned original would likely realize approximately $25–60M, subject to deaccession and legal constraints.

$20-60 million

MoMA’s large 1927 The Menaced Assassin, despite museum provenance and exhibition history, would—if ever offered—most plausibly sell in the $20–60M range based on comparables.

$30-50 million

Sotheby’s achieved $26,830,500 for Le Principe du plaisir in 2018; adjusting for subsequent market movement and comparables places its current auction potential at roughly $30–50M.

$20-40 million

If the canonical 1937 oil La Reproduction interdite, it would be estimated at $20–40M; later studio versions, prints, or heavily restored examples would fall to about $0.5–5M.

$10-40 million

MoMA’s canonical 1928/29 The False Mirror is not market‑traded; a museum‑quality, firmly attributed oil would defensibly be priced at approximately $10–40M.

Market Context

René Magritte occupies a blue‑chip, bellwether position in Surrealism, with deep global demand from cross‑category collectors and major museums; his auction record was re‑set at $121.16 million for L’empire des lumières (Christie’s New York, Nov 19, 2024), following a prior high of ~ $79.8 million (Sotheby’s, 2022) and strong mid‑tier results including $43.2 million in 2024 for L’ami intime. Supply of prime oils is constrained, institutional programming and the 2024 centenary have concentrated buyer interest, and houses increasingly deploy third‑party guarantees and single‑owner evening‑sale strategies. The market shows a flight to quality—canonically iconic, well‑provenanced works command premiums and resilient liquidity at the top while mid‑market material remains selective and estimate‑sensitive.