Most Expensive Jean-Auguste-Dominique Ingres Paintings

Jean-Auguste-Dominique Ingres occupies a unique position in the market as both a canonical Neoclassical master and an artist whose rarity and impeccable provenance make individual canvases highly collectible; at the apex sit the sensual exotica of Grande Odalisque (estimated $150–300 million) and the closely related The Great Odalisque (listed at $200–300 million), whose sumptuous surfaces, elongated forms and storied ownership histories drive speculative demand. Equally prized are his commanding portraits—Portrait of Madame Moitessier and Portrait of Monsieur Bertin, each valued around $100–150 million—for their virtuoso draftsmanship and the sitter’s social cachet. Monumental allegories and historic scenes such as The Apotheosis of Homer ($30–80 million), Oedipus and the Sphinx ($15–60 million) and The Vow of Louis XIII ($15–60 million) attract institutional buyers for their cultural significance, while The Turkish Bath ($20–60 million), Portrait of the Princesse de Broglie ($20–50 million) and The Valpinçon Bather ($15–50 million) appeal to collectors drawn to Ingres’s blend of polished finish, sensuous line and scarcity on the market, factors that together sustain his premium valuations.

$150-300 million

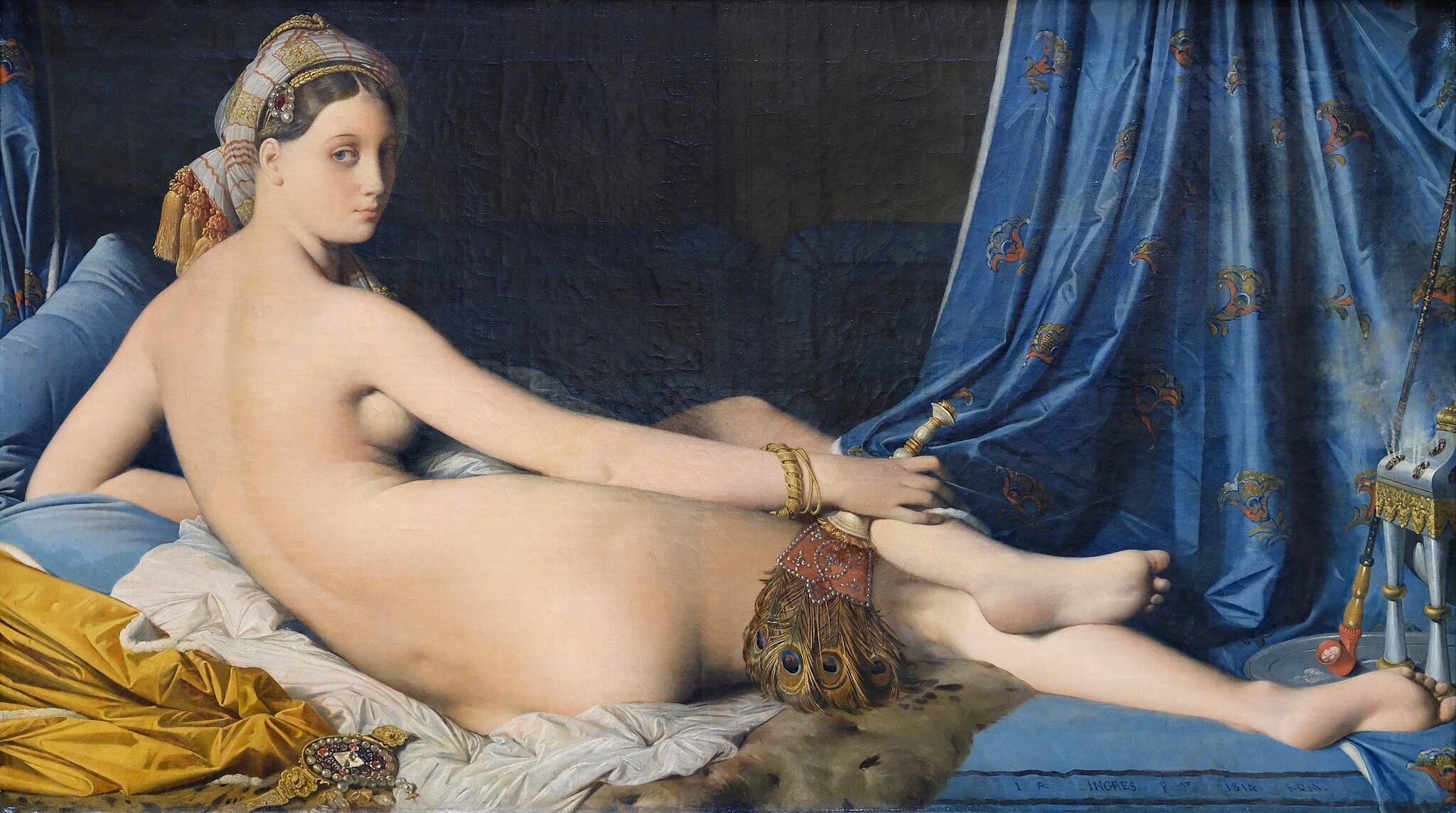

A hypothetical open‑market estimate of $150–300 million reflects La Grande Odalisque’s apex status in Ingres’s oeuvre, extreme scarcity of comparable oils, and trophy Old Master benchmarks.

$200-300 million

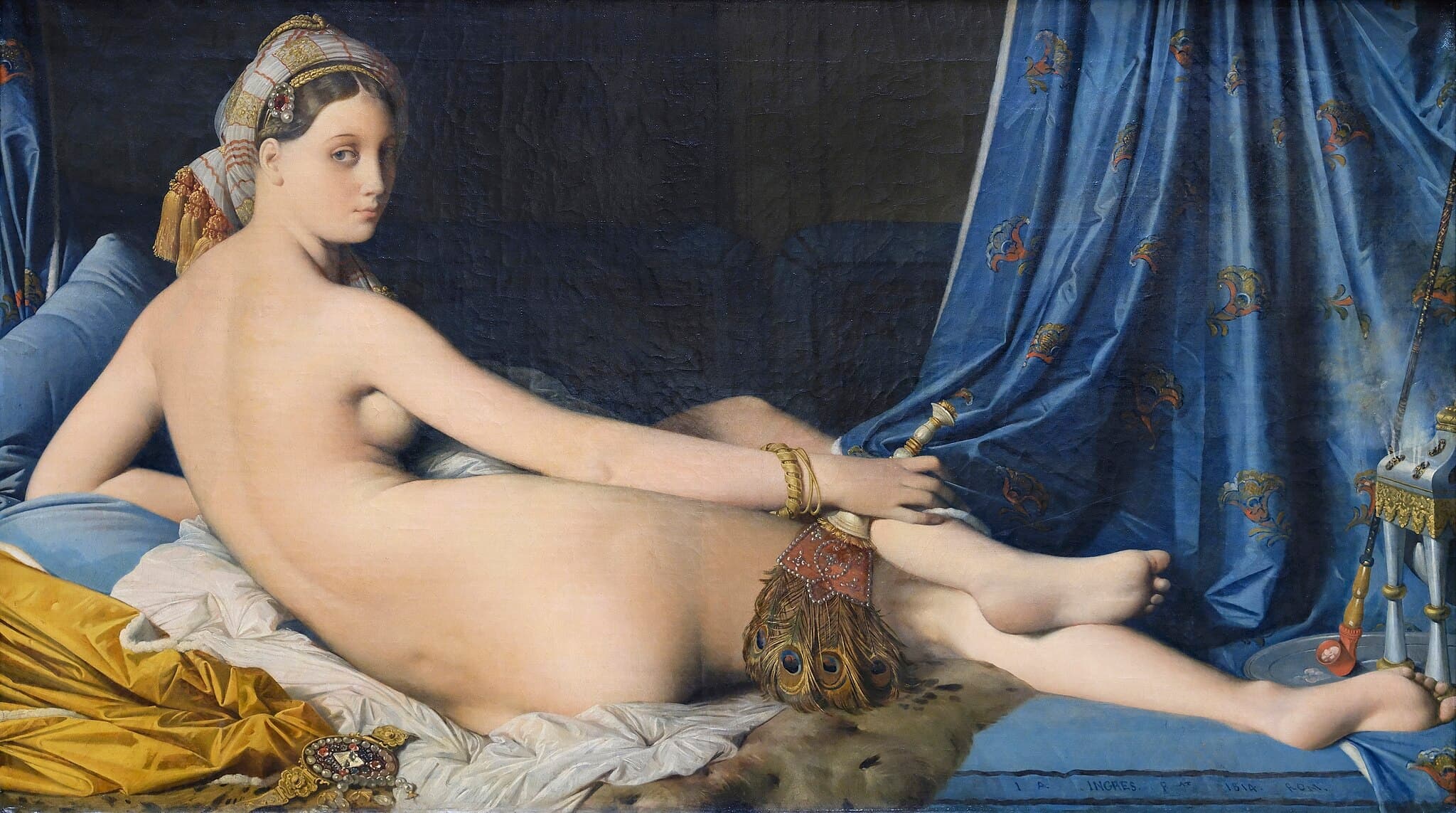

Insured/indemnity proxy of $200–300 million because The Great Odalisque is inalienable in the Louvre, so any value is a theoretical insurance estimate rather than a sale price.

$100-150 million

Projected $100–150 million range is a market proxy for Portrait of Madame Moitessier (National Gallery) — a canonical, museum‑held masterpiece effectively unavailable for sale.

$100-150 million

Estimated insured/replacement value of $100–150 million for Portrait of Monsieur Bertin (Louvre) contrasts with a plausible hypothetical auction band of about $20–60 million.

$30-80 million

A reasoned market proxy of $30–80 million for The Apotheosis of Homer (Louvre) reflects its monumental scale, trophy premiums and legal/institutional protections that keep it off the market.

$20-60 million

A counterfactual auction estimate of $20–60 million for The Turkish Bath (Le Bain turc) assumes an autograph, museum‑quality tondo and is driven by provenance and top‑end French Old Master comparables.

$15-60 million

If the 1824 Vœu de Louis XIII is an autograph, large‑scale museum‑quality oil its theoretical market value is $15–60 million; a study or workshop version would be roughly $200K–$2M.

$15-60 million

If an autograph full‑scale oil by Ingres, Oedipus and the Sphinx is estimated at $15–60 million; any attribution, provenance or condition downgrade would materially reduce that range.

$15-50 million

A theoretical $15–50 million band for The Valpinçon Bather (Louvre) treats it as a marketable, pristine Ingres oil, with value highly sensitive to legal, condition and provenance constraints.

$20-50 million

Hypothetical open‑market valuation of $20–50 million for Portrait of the Princesse de Broglie reflects its museum‑quality status (Met) and extreme scarcity of finished Ingres oils on the market.

Market Context

Jean‑Auguste‑Dominique Ingres’s auction market is defined by extreme scarcity of fully autograph major oils—most canonical canvases sit in museums—so public turnover is dominated by drawings and studies (top sheets approaching $2m) while oil sale records remain in the low single millions (notably Portrait de la comtesse de La Rue, €2.081m, Christie’s Paris 2009; a small Odalisque variant $1.71m in 2020). Recent marquee Old Master results (e.g., Botticelli’s $92.2m, France’s €26.73m Chardin, and high‑profile drawings) show strong cross‑category appetite for museum‑caliber works, but Ingres’s market is bifurcated: deep, institutional and advanced‑connoisseur demand at the top versus thin liquidity and selective mid‑market interest. Valuations for a transferable major Ingres therefore rely on trophy comparables, pristine provenance, and competitive cross‑category bidding.