How Much Is Ancient Greece and Egypt Worth?

Last updated: April 14, 2026

Quick Facts

- Methodology

- comparable analysis

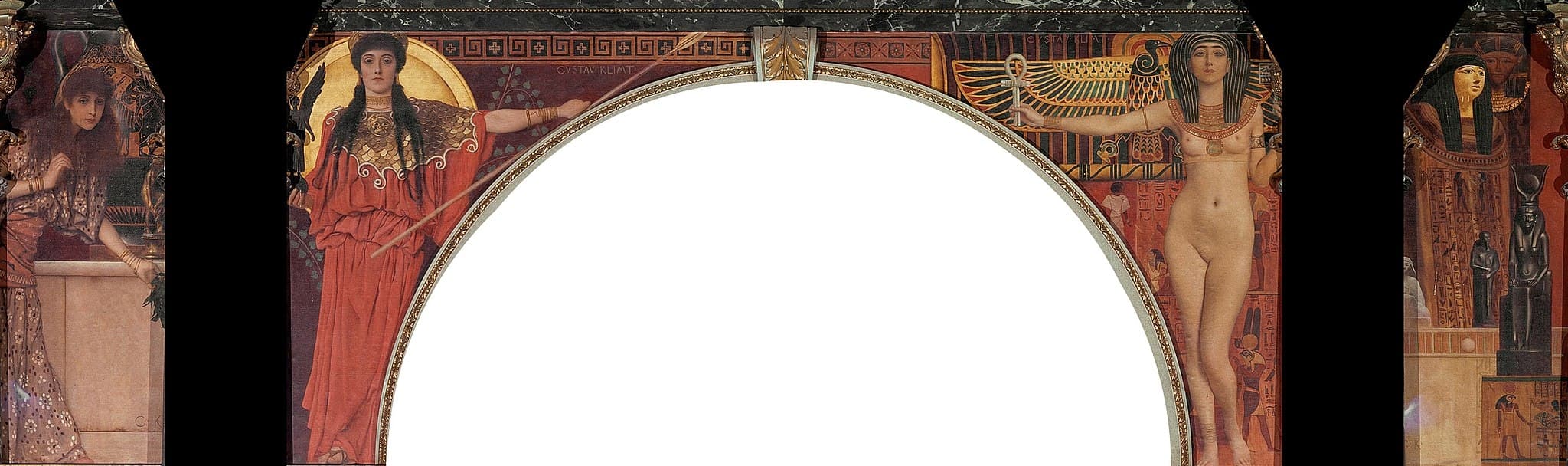

Ancient Greece and Egypt is an early, in-situ decorative panel by Gustav Klimt within the Grand Staircase of Vienna’s Kunsthistorisches Museum. It has never been on the market and is effectively non‑transferable, but on a fully hypothetical, deaccessioned and exportable basis, we estimate $18–30 million. The range reflects Klimt’s powerful brand and recent record prices, offset by the work’s early, programmatic nature and severe legal/physical constraints.

Ancient Greece and Egypt

Gustav Klimt, 1891 • Oil on canvas

Read full analysis of Ancient Greece and Egypt →Valuation Analysis

Object and context. Ancient Greece and Egypt forms part of Gustav Klimt’s early decorative cycle for the Grand Staircase at the Kunsthistorisches Museum (KHM), Vienna, executed c. 1890–91 within the Künstler‑Compagnie commission. It is an in‑situ, programmatic oil on canvas designed for a specific architectural setting and, as such, has never been offered on the open market and is effectively non‑market under normal circumstances [1].

Method and benchmark pricing. This valuation synthesizes recent, top‑tier Klimt auction benchmarks with discounts appropriate to an early, site‑specific, collaborative decoration. Klimt’s market has reset upward: Portrait of Elisabeth Lederer achieved about $236.4m at Sotheby’s New York in November 2025, establishing the artist’s auction record and confirming extraordinary demand when quality, rarity, and provenance align [2]. Lady with a Fan made c.$108.4m in London in 2023 [3], while the prime landscape Birch Forest realized c.$104.6m in 2022 [4]. These results define the ceiling for late portraits and first‑tier landscapes.

Position within the oeuvre; discounts applied. By contrast, Ancient Greece and Egypt is an early, academic‑historicist, programmatic panel executed for a state commission. It lacks the autonomous, late stylistic hallmarks (gold ground, mosaic surface, or fully developed Secessionist idiom) prized by private collectors. It is also embedded in an architectural ensemble, complicating removal, display, and conservation. Finally, authorship within the staircase cycle, though credited to Gustav Klimt, sits within the Künstler‑Compagnie framework, which can introduce attributional nuance relative to fully autographic easel paintings. These factors warrant a substantial discount to late portraits and prime landscapes.

Legal and practical constraints. Austrian cultural‑property and monument‑protection regimes require export licenses for protected works; permissions can be denied to safeguard national heritage, and in‑situ museum decorations face formidable hurdles. Such legal frictions narrow the buyer pool, reduce liquidity, and suppress pricing even in a hypothetical sale scenario [5]. Physical removability, structural condition, past restorations, and installation method would further influence cost, risk, and therefore value.

Conclusion and range. Balancing Klimt’s exceptional brand strength and the scarcity of any oil‑on‑canvas by the artist against the object’s early, programmatic character, collaborative context, in‑situ status, and legal/export constraints, we estimate a fully hypothetical market value of $18–30 million, assuming (1) lawful deaccession, (2) safe, conservation‑sound removal, (3) clear, primarily autographic authorship by Gustav Klimt, and (4) exportability. A pristine technical report and clean title could push the work toward the high 20s; significant removability risk, mixed authorship, or export barriers would press the outcome toward the lower end of the range [1–5].

Key Valuation Factors

Art Historical Significance

High ImpactAs part of the KHM Grand Staircase cycle, Ancient Greece and Egypt occupies a formative place in Klimt’s career and Vienna’s Ringstrasse‑era monumental decoration. It demonstrates the artist’s pre‑Secession, academic approach and his early mastery of large‑scale architectural programs. Scholarly and institutional relevance is therefore strong: the panel contributes to understanding how Klimt evolved toward his later, iconic idiom, and it belongs to a celebrated Gesamtkunstwerk familiar to millions of museum visitors. While market value is partly driven by private‑collector appeal (where late portraits and prime landscapes dominate), the object’s institutional and educational importance remains indisputable. This significance underpins a robust baseline of demand in any hypothetical sale, especially among museums and culturally motivated buyers, even as its decorative, programmatic nature limits trophy‑level private competition.

Position in the Oeuvre and Collector Demand

Medium ImpactRelative to the late portraits and prime landscapes that command Klimt’s highest prices, this early, programmatic panel sits lower in the desirability hierarchy. Collectors pay a premium for the artist’s mature style—golden surfaces, symbolic iconography, and autonomous, exhibition‑scale canvases with iconic name recognition. By comparison, a staircase panel in an academic‑historicist manner, even when largely autographic, is seen as secondary to the artist’s mature masterpieces. That said, the Klimt name exerts a powerful pull, and scarcity of any oil by Klimt sustains substantial interest. The result is a meaningful but measured range: serious connoisseurs and institutions would bid, but the bidding climate would be more selective and price‑sensitive than for late portraits, keeping values well below triple‑digit millions.

Legal/Heritage and Export Constraints

High ImpactAustria’s cultural‑property framework can restrict deaccession and export of nationally significant works. An in‑situ, commissioned museum decoration would face especially rigorous scrutiny. Even in a scenario where deaccession were permitted, obtaining an export license might be challenging or impossible, and any restrictions (e.g., retention in Austria or non‑export status) would materially shrink the buyer pool and depress price. Global bidders typically demand frictionless title and international portability for eight‑figure purchases; uncertainty here translates directly into discounts or failed transactions. Accordingly, legal feasibility and exportability are value‑critical: a confirmed ability to remove and export the panel could support the upper end of the estimate, while constraints would push toward the lower end—or foreclose a sale entirely.

Format, Condition, and Removability

Medium ImpactThe panel’s architectural integration raises practical issues absent from standard easel paintings. Its structural mounting, canvas supports, and historic interventions must be assessed to determine whether safe, reversible removal is possible without loss. Complex deinstallation, conservation risk, and high costs reduce net realizable value and can deter private buyers without institutional conservation capacity. By contrast, a positive condition report—stable support, reversible installation, minimal prior restoration—would mitigate risk and support pricing. Display adaptability also matters: works designed for a specific architectural context can be difficult to integrate into private settings, dampening demand. In short, technical feasibility and conservation risk are among the most material, actionable variables in the valuation and would meaningfully influence auction estimates and reserves.

Attribution and Workshop Participation

Medium ImpactWhile the staircase program is broadly credited to Klimt within the Künstler‑Compagnie (with Ernst Klimt and Franz Matsch), value will hinge on how fully autographic this specific panel is considered. Clear documentation that Ancient Greece and Egypt is principally by Gustav Klimt, with minimal workshop intervention, supports stronger pricing. Any ambiguity introducing significant workshop execution, shared authorship, or restitution‑sensitive provenance would suppress demand and invite heavier discounting. Conversely, high‑quality technical imaging, archival documentation, and connoisseurship attesting to Klimt’s hand would bolster confidence and price. In the current market—heightened for due diligence—auction houses and buyers will insist on definitive authorship statements and robust cataloguing before committing to upper‑range bids.

Sale History

Ancient Greece and Egypt has never been sold at public auction.

Gustav Klimt's Market

Gustav Klimt is a blue‑chip, trophy‑artist with exceptionally deep global demand and chronically limited supply. The market reset higher in 2025 when Portrait of Elisabeth Lederer brought roughly $236.4m at Sotheby’s New York, establishing a new artist auction record and reaffirming appetite for late, iconic works. Other recent benchmarks include Lady with a Fan at about $108.4m (London, 2023) and the landscape Birch Forest at approximately $104.6m (New York, 2022). First‑tier landscapes routinely command eight‑figure prices, and mature portraits can exceed $100m, with pristine provenance and museum‑caliber quality drawing the widest participation. Early, academic‑period works and decorative projects trade well below the top tier but still benefit from Klimt’s brand strength and rarity.

Comparable Sales

Insel im Attersee (Island in the Attersee)

Gustav Klimt

Same artist; blue‑chip oil painting used to calibrate pricing for Klimt oils even though subject/type differ. Within roughly a decade of the KHM staircase project; shows market appetite for non‑portrait Klimts.

$53.2M

2023, Sotheby's New York

~$56.3M adjusted

Birch Forest

Gustav Klimt

Same artist; major landscape oil. Calibrates the upper end for important non‑portrait Klimts—useful when discounting a site‑specific, programmatic early decoration.

$104.6M

2022, Christie's New York

~$115.7M adjusted

Lady with a Fan (Dame mit Fächer)

Gustav Klimt

Same artist; late portrait that set the European auction record (2023). Serves as a top‑of‑market benchmark versus which an early, architectural decoration would be heavily discounted.

$108.4M

2023, Sotheby's London

~$114.8M adjusted

Portrait of Elisabeth Lederer

Gustav Klimt

Same artist; 2025 auction record for Klimt and for any Modern artwork. A ceiling benchmark highlighting the premium for late, iconic portraits versus early decorative, in‑situ works.

$236.4M

2025, Sotheby's New York

Portrait of Fräulein Lieser

Gustav Klimt

Same artist; late, unfinished portrait with provenance questions. Hammered at ~€30m (≈$37.5m with fees) but the sale later collapsed; still a useful indicator for non‑trophy Klimt pricing. An early, in‑situ museum decoration would likely sit below this.

$37.5M

2024, im Kinsky, Vienna

~$38.6M adjusted

Litzlberg am Attersee

Gustav Klimt

Same artist; prime restituted landscape. Adjusted to 2025, it implies c.$58m for top‑tier Klimt landscapes—an anchor for discounting a collaborative, site‑specific early panel.

$40.4M

2011, Sotheby's New York

~$58.3M adjusted

Current Market Trends

The Modern and Impressionist segment rebounded in 2025 after a selective 2023–2024, with New York anchoring top‑end performance and trophy lots outperforming the broader market. Klimt’s record‑setting portrait led this recovery, while strong results for prime landscapes confirmed depth beyond a single masterpiece. Buyers are highly discriminating: they reward impeccable provenance, marquee quality, and exhibition visibility, and they penalize legal friction or condition risk. Viennese Secession material remains culturally salient through exhibitions and restitution narratives, sustaining attention across the category. In this environment, an early, programmatic Klimt would see solid institutional and connoisseur demand but remain priced below late portraits and premier landscapes—especially if subject to export constraints or complex deinstallation.

Study print

Study this painting as a print

Pair the full artwork with a museum-style study sheet focused on one meaningful detail.

Sources

- Kunsthistorisches Museum Wien – The Kunsthistorisches Museum as a Gesamtkunstwerk

- Sotheby’s – The New York Sales, November 2025 (Breuer) Results

- Forbes – Gustav Klimt’s Final Portrait Sells For A Record $108.4 Million In London

- Christie’s Press – The Paul G. Allen Collection totals $1.62 billion

- Bundesdenkmalamt (Austria) – Export of Cultural Property