How Much Is No. 7 Worth?

Last updated: May 11, 2026

Quick Facts

- Last Sale

- $82.5M (2021, Sotheby's New York (The Macklowe Collection))

- Methodology

- extrapolation

Fair‑market opinion for Mark Rothko’s No. 7 (1951): $100–150 million, assuming excellent condition, clear title and sale via a high‑end private or institutional channel. This band is anchored to the confirmed Sotheby’s Nov 15, 2021 sale (~$82.5M) and adjusted upward based on subsequent private‑sale precedent and current market structure.

Valuation Analysis

Valuation conclusion: I estimate Mark Rothko's No. 7 (1951) to have a fair‑market value between $100,000,000 and $150,000,000, assuming excellent condition, clear legal title, and sale via a high‑end private or institutional channel. This opinion applies an extrapolation methodology: it is anchored to the confirmed Sotheby's sale of this exact canvas on 15 November 2021 (reported final price ≈ $82.5M; hammer ≈ $77.5M) and adjusts that anchor to reflect subsequent private‑sale precedent, market structure and scarcity of similarly documented 1951 Rothkos. The approach blends direct sale evidence with observed top‑end private transactions and present‑day demand indicators to produce a practical market band [1].

The 2021 Sotheby's lot is a primary market anchor because it documents the work's catalogue raisonné entry (David Anfam no. 455), dimensions and a blue‑chip provenance that traces to Betty Parsons, the Blaffer Foundation and Pace — attributes that materially reduce attribution and title risk and increase institutional interest [1]. Works from this transitional 1951 period are especially prized by museums and private collectors for their art‑historical placement in Rothko's development toward the mature multiform fields. Given the painting's large scale (≈240.7 x 138.7 cm) and clear documentation, it sits above ordinary mid‑1950s comparables in collectability and is thus more likely to command a premium in a competitive sale environment.

Significant private‑sale evidence since 2021 supports lifting the upper bound of a valuation range: Christie's reported an early‑2024 private transaction in excess of $100M for a Rothko, demonstrating that motivated buyers will transact above public auction levels when exclusivity, timing and certainty are provided [2]. Auction houses increasingly route canonical, high‑value Rothkos through private‑sale desks or guaranteed offers, concentrating nine‑figure liquidity off‑block. For this canvas, such a private placement — or a well‑structured guaranteed auction with active marketing and institutional outreach — can realistically achieve figures toward the top of the stated band.

Equally, public‑sale risk and recent geographic softness temper headline upside: several noteworthy Rothko canvases offered publicly since 2022 have produced mixed results, and regional differences (for example, certain Asia offerings) have shown material dispersion versus prior highs, a sector‑level pattern documented in contemporary market reports [3]. The lower edge of $100M assumes a strong private buyer or a successful guaranteed process; the midpoint and upper edge ($125M–$150M) require multiple competitive bidders or a buyer with mission‑driven institutional intent and minimal title/condition contingencies.

Practical caveats and next steps: finalize the valuation by obtaining high‑resolution images, a current conservator's condition report, the Anfam RA pages and complete title paperwork. Any condition issues, conservation history, encumbrances or export restrictions will materially move the opinion. If you want a sale recommendation, I advise prioritizing a controlled private‑sale program or a guaranteed sale with active institutional outreach rather than an unstructured evening‑sale consignment; that sales route best captures the nine‑figure buyer pool that drives the upper band.

Key Valuation Factors

Art Historical Significance

High ImpactThe painting's 1951 date places it at a critical juncture in Rothko's development from figuration and early experiments to his mature color‑field compositions. Works from this year are closely studied by scholars and curators because they demonstrate compositional and chromatic decisions that prefigure his canonical style. If the canvas corresponds to Anfam no. 455 and displays the large vertical multiforms typical of Rothko's breakthrough period, its art‑historical importance is high. High significance increases museum interest and collector competition, supporting both price resilience and the ability to approach or exceed nine‑figure outcomes in the right sales channel.

Provenance & Exhibition History

High ImpactProvenance is a principal value driver for top‑end Rothkos. This work's documented chain — Betty Parsons representation, institutional stewardship (Blaffer Foundation), Pace commercial handling and Macklowe ownership — materially reduces attribution and title risk and widens the buyer universe to institutions. Exhibition and publication history further validate the canvas for curators and trustees and shorten marketing cycles. Strong, uninterrupted provenance and catalogue raisonné citation increase the probability of institutional bids or competitive private offers; any gaps or disputes would materially lower marketability and require a discount, particularly at nine‑figure levels.

Condition & Conservation

High ImpactCondition frequently controls realizable value for Rothko canvases. Structural problems (tears, compromised supports), heavy relining, pervasive inpainting or unstable pigments can reduce buyer confidence and prompt discounts of tens of percent among top buyers. Conversely, a recent conservator's report confirming stable support, minimal intervention and intact surface structure materially supports the upper valuation band. Buyers at the highest tier expect full disclosure; absence of a current, professional condition report will increase perceived risk and lower the achievable price in both private and public sale contexts.

Sale Channel & Market Liquidity

High ImpactThe chosen sales route is decisive. Nine‑figure Rothko transfers are increasingly executed privately or via guaranteed auctions with targeted outreach; the reported Christie’s private sale above $100M is a clear example of off‑block liquidity. Private placements capture confidentiality, buyer certainty and reduced execution volatility, often producing premiums over public results. In contrast, an unprotected evening auction introduces execution risk (guarantee terms, irrevocables, buyer fatigue) that can compress outcomes. For this canvas, a controlled private placement or a guaranteed auction with institutional marketing maximizes the chance of achieving the high end of the band.

Legal, Title & Export Concerns

Medium ImpactClear title and exportability are prerequisites for full market value, especially for institutional buyers. Any encumbrances, unresolved restitution claims, tax liens or incomplete export documentation will deter conservative buyers and can materially depress price or derail transactions. At the nine‑figure level, buyers conduct intensive legal due diligence; sellers must deliver complete provenance and title paperwork. The existence of clean, transferable title supports cross‑border institutional interest and preserves the full market band, while unresolved legal issues can necessitate steep discounts or protracted sale timelines.

Sale History

Sotheby's New York (The Macklowe Collection)

Mark Rothko's Market

Mark Rothko remains a top‑tier, blue‑chip figure in the post‑War market: canonical 1950s canvases are institutionally validated, scarce in private hands and therefore highly sought. Auction records and high‑profile private transactions demonstrate both sustained demand and a bifurcated market structure: public auctions capture many comparables while nine‑figure transactions increasingly occur privately. While mid‑market Rothkos exhibit volatility, museum‑quality, well‑provenanced works from Rothko's mature period continue to attract deep pockets and institutional interest, underpinning long‑term value even as short‑term public results vary.

Comparable Sales

Orange, Red, Yellow

Mark Rothko

Artist benchmark and auction high-water mark (1961 work); large, museum-quality Rothko used as the top-end reference.

$86.9M

2012, Christie's New York

~$122.5M adjusted

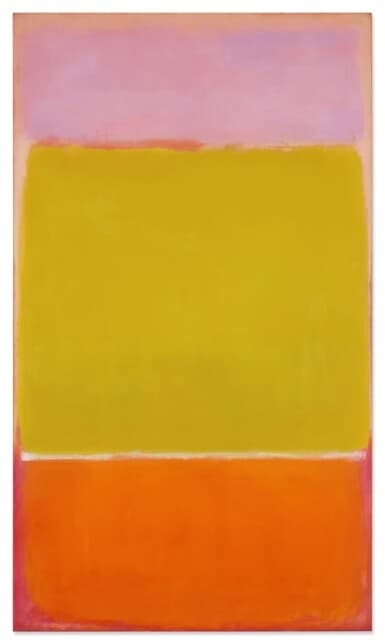

No. 7

Mark Rothko

Subject painting's confirmed public-auction result — the best direct market anchor for this exact canvas and provenance.

$82.5M

2021, Sotheby's New York (The Macklowe Collection)

~$98.5M adjusted

Untitled (Yellow, Orange, Yellow, Light Orange)

Mark Rothko

Large mid‑1950s Rothko sold recently at public auction — good period/scale comparable showing mid-market prices for 1950s canvases.

$46.4M

2023, Christie's New York

~$49.2M adjusted

Untitled (Yellow and Blue)

Mark Rothko

Mid‑1950s Rothko sold in Asia — useful for geographic/market-channel comparison; shows regional pricing variation and relative softness vs prior highs.

$32.5M

2024, Sotheby's Hong Kong

~$33.3M adjusted

Rothko (Macklowe Collection, different canvas)

Mark Rothko

Another Rothko from the same Macklowe dispersal — useful to assess how works from the same collection performed across consecutive sales.

$48.0M

2022, Sotheby's New York (The Macklowe Collection sale)

~$53.0M adjusted

Current Market Trends

Since 2021 the market has bifurcated: private sales dominate top‑end transfers while public auctions show greater dispersion. Macro volatility and regional softness have tempered some auction outcomes, but major retrospectives and concentrated private buying power sustain demand for canonical works. Auction houses increasingly use guarantees and private‑sale desks to manage risk; for Rothko this favors private or guaranteed strategies to realize nine‑figure results.